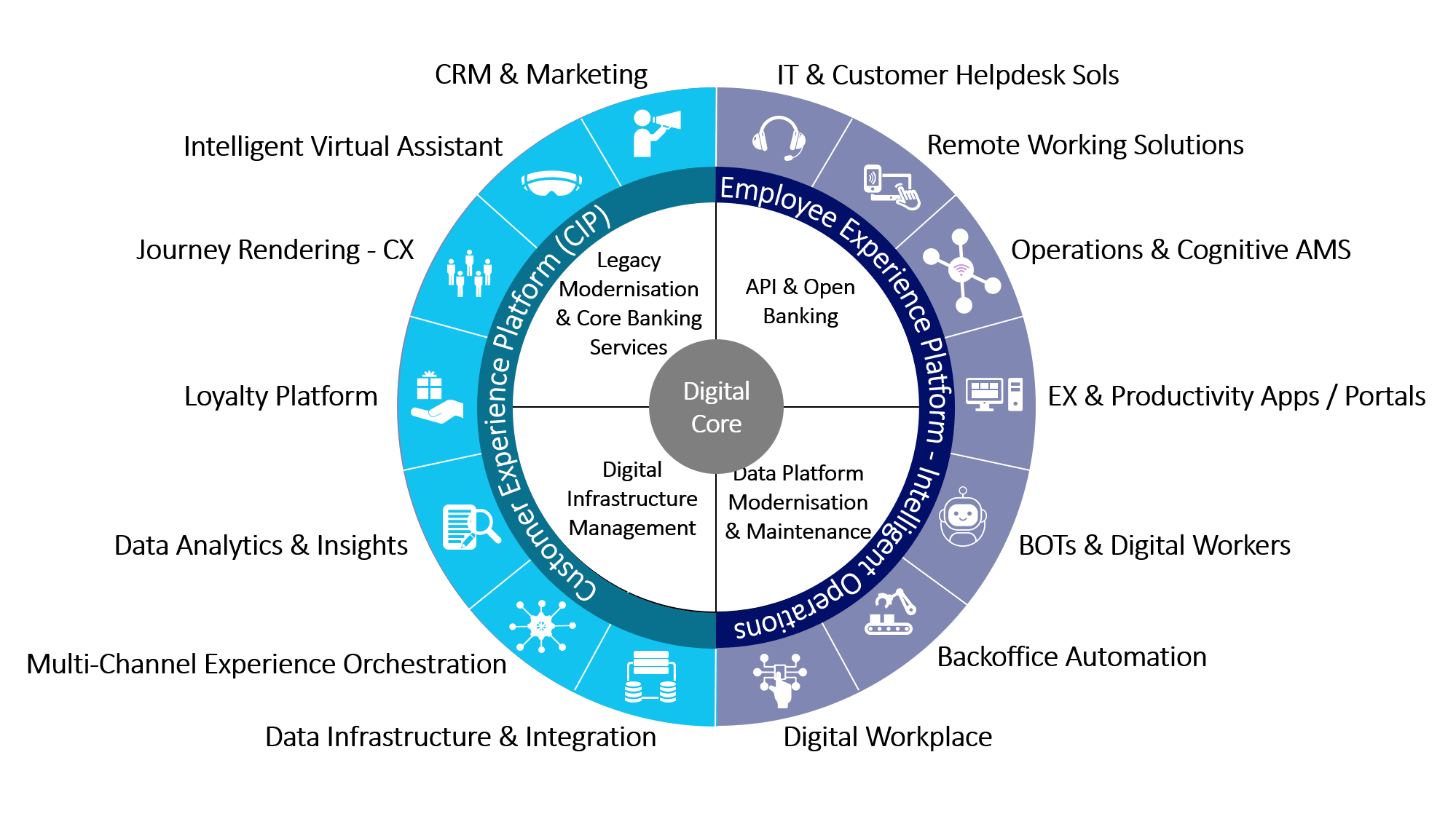

One of the strategic focus areas of ITC Infotech is providing business-friendly solutions for Digital Banking. It covers the landscape across customer experience, Digital Operations & employee experience, and Digital Foundation, which includes Data & Core modernisation. We are constantly shaping and calibrating our POVs and offerings, working closely with our clients and prospects.

Over the years, we have come across many clients, both traditional and FinTechs, who are facing tremendous challenges with their legacy mainframe-based core banking platform. They are neither able to launch any new industry leading customer experience solutions, nor able to bring out any innovative propositions to remain competitive in the marketplace.

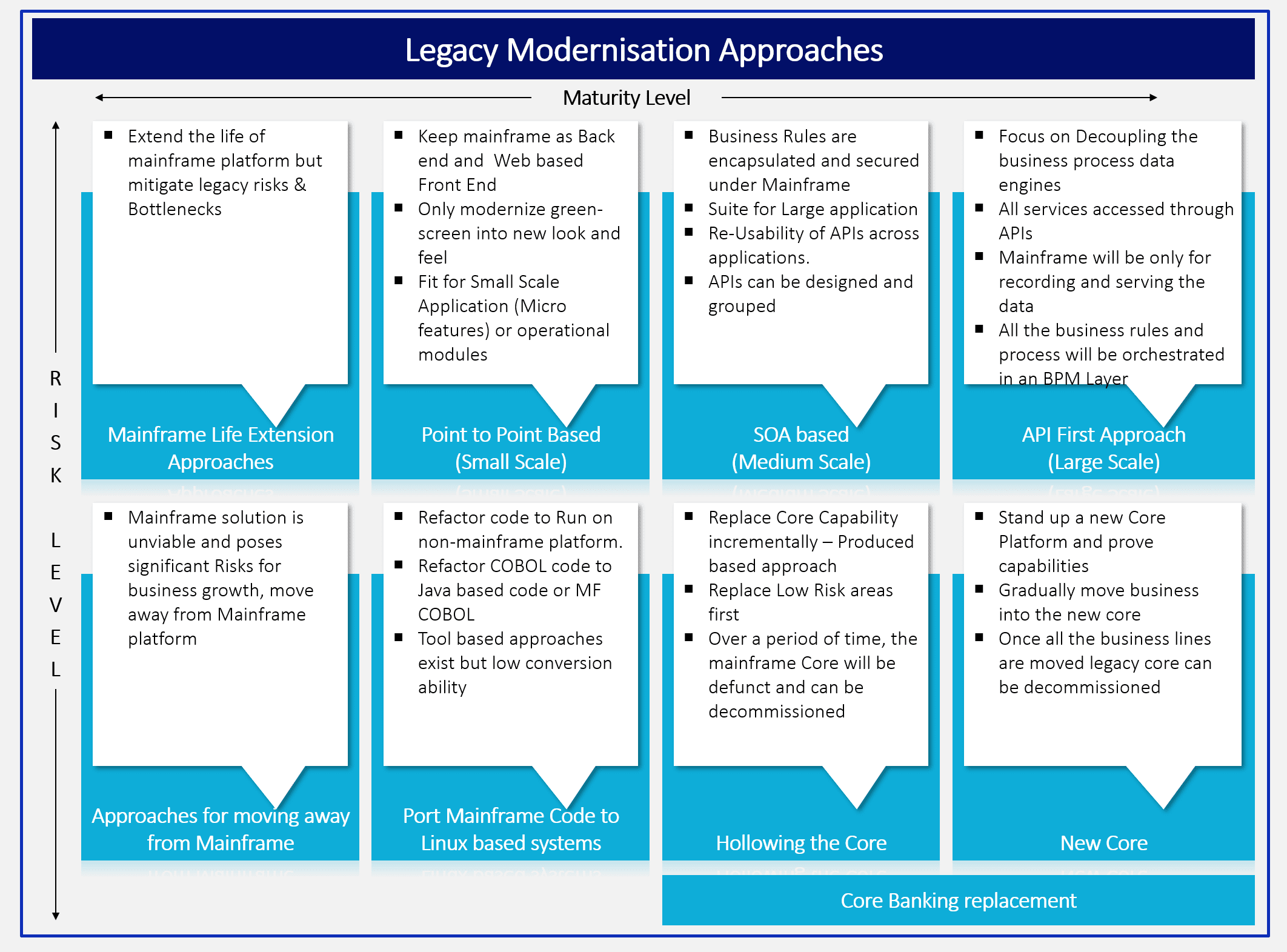

Generally, there are two broad approaches that we have seen and have worked on –

- Extend the life of the legacy/mainframe – Continue to use mainframe platform but mitigate legacy risks & Bottlenecks

- Move away from Mainframe completely – Mainframe solution is unviable and poses significant Risks for business growth.

Customers adopt their approach primarily based on the transformation drivers – Cost pressures, business imperatives and/or risk appetite.

Extending life of Legacy

An organisation pursues this approach if the primary driver for transformation is to resolve Digital Laggardness or enable business innovation. Under this approach, the legacy continues but specific interventions are brought in to enable or build new age Digital experience to customer and employees alike. Most common approach is to gradually move to an API first model. The bulk of Business rules and the entire data continue to reside on legacy. Many use this opportunity to also look at ways of reducing MIPS cost (in case of mainframes) by externalising data to an ODS. There are typically three variants as far as this approach goes –

- Point to point API enablement – Overarching strategy is to keep mainframe as Back end and use Web based Front End, by modernizing green-screen to deliver new experience to Suitable only for Small Scale Application (or operational modules.

- SOA Based Componentization & API Enablement – The entire monolith is componentised into SoX (SoR, SoI, SoE) and is suitable for larger application and more detailed API enablement which extend to Customer Experience layer.

- API First approach – most complex and mature strategy which focusses on de-coupling business rules and data processing. End to end API enablement means that all functions and services are accessed through APIs across the board – internal and external. BPM tools are used to orchestrate the business processes and Mainframe only performs data crunching & storage.

Moving away from Mainframe

This approach is normally adopted if the legacy platform limits opportunities for API enablement and/or legacy (mainframe in many instances) costs are way too high. Now, the biggest risk with this approach is that business is running, in many cases there are multiple brands enabled on the same code base so one easy approach at least in theory to mitigate some of the operational risk is to keep the business rules, data structures intact and move the code as-is to a Linux platform. There are tools which can help to convert/refactor code to today’s most popular option – Microfocus COBOL on Linux. However, this approach has advantages and disadvantages:

- The advantage – The business roles and data structures remain unchanged and only the underlying infrastructure is impacted in theory – which is less risky.

- The disadvantage – All the inherent issues & bugs in legacy code gets carried forward to new infrastructure and opportunity to refactor is missed. This needs to be resolved before porting the code.

The riskier approach is replacing the core platform with a Commercial off-the-shelf (COTS) Core Banking product. This can be done multiple ways, by either gradually replacing a set of core functionalities of a period of time, thereby eventually making the mainframe code redundant – commonly termed as hollowing the core or standing up a brand new system in parallel, now a days entirely on the cloud, and to move business lines to the new core over a period of time.

Conclusion

There is no one size fits all option that is available but we believe that while the mainframe extension approach and the porting COBOL code to Linux platform might look like a good strategy in the short term, organisations need to definitely think about moving away from the legacy code. While the cost savings, and the infra evergreening are the most tangible outcomes, significant risk persists i.e. inherent code issues in the mainframe code, undocumented business rules, niche skills availability to name a few and therefore the banks will be better off to moving to a scalable cloud based, API and Digital first architecture.

ITC Infotech brings years of experience

ITC Infotech provides end to end Digital Banking Solutions and one of the core areas is our Legacy & Core modernisation services. ,Regardless of the approach, we can help enterprises embark on a successful journey from Monolith to Microservices.. Equally, our DX practice focusses on Data Modernisation & Analytics led CX solution framework, we call it the Customer Intelligence Platform for Banking.

If you are looking to move to an industry leading Core Platform, our deep specialisation can come handy. ITC Infotech is a Platform Agnostic Core Banking Services provider and our Retail & Corporate Banking CoE allows us to build and scale this capability around a number of industry leading Core Platforms. We offer end to end services required for implementation of a new core platform – from Business Analysis, Design, Development, testing to implementation & support services. Please contact us to know more about our services and offerings.

Authors:

Ranjith Ranadheeran

GM – Banking and Financial services

Recent Posts

PPWR Compliance Will Fail Without SKU-Level Packaging Data. Is your Company ready?

PPWR Compliance Will Fail Without SKU-Level Packaging Data. Is your Company ready?- Why Disconnected Packaging Data Could Become the Biggest PPWR Risk for CPG Companies

From Spending to Scaling: Architecting AI for Sustainable Business Value

From Spending to Scaling: Architecting AI for Sustainable Business Value From Signed to Sellable: The New Benchmark for Hotel Onboarding

From Signed to Sellable: The New Benchmark for Hotel Onboarding Architecting the Frictionless Guest Journey Through Agentic AI

Architecting the Frictionless Guest Journey Through Agentic AI